Blogs

Tax Saving Tips: How NPS Helps You Reduce Your Tax Burden

With the recently rising global uncertainties, wise tax planning can effectively result in enhanced financial security.

NPS (National Pension System) with its diverse NPS schemes have emerged as a popular investment to improve retirement preparedness and deliver considerable tax saving benefits.

Disciplined contribution to an NPS Tier-I account can help taxpayers leverage a combination of statutory deductions and a suitable tax treatment at maturity. The NPS scheme investments can thus, collectively help reduce their annual tax burden.

With this dual role, NPS can be a strategic retirement asset and a better tool to income tax saving. Here is more on the role of an NPS scheme in tax saving.

The Three Pillars of Savings

An NPS scheme’s tax saving framework revolves around three major sections of the Income Tax Act.

Section 80CCD (1) - Individual contributors can claim a deduction on their own NPS contributions up to 10% of salary (Basic plus Dearness Allowance). However, this deduction is subject to the overall ceiling of ₹1.5 lakh under Section 80CCE.

Section 80CCD(1B) - Additionally, with Section 80CCD(1B) investors can avail of an exclusive deduction of up to ₹50,000 for self-contributions to a Tier-I account, over and above the 80CCE limit.

Section 80CCD(2) - With this section, NPS scheme investors get an additional deduction for employer contributions up to 10% of the employee’s salary. This deduction is 14% for central government employees, without affecting the ₹1.5 lakh limit.

These three provisions can together offer the “triple tax benefit” to NPS scheme subscribers.

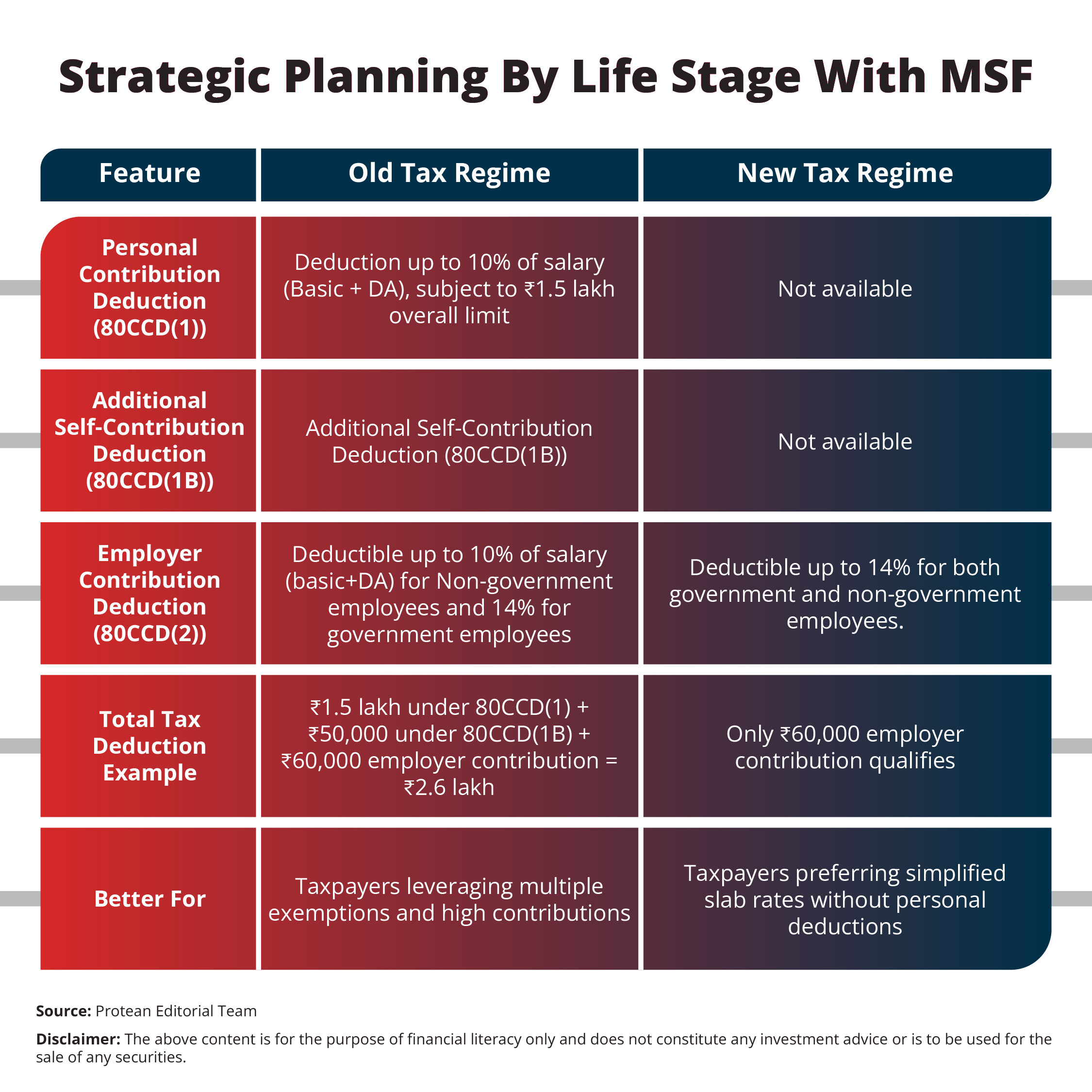

NPS in 2026: Old vs. New Tax Regime Comparison

The tax benefits of NPS differ depending on whether a taxpayer opts for the old or new tax regime.

Here is a comparison table summarising the Old vs New tax regime differences clearly.

Disclaimer: The comparison in the above table shows how selecting the right regime can help NPS subscribers maximise tax benefits while planning for retirement.

The EEE Advantage

NPS scheme investments in Tier-I have the EEE (Exempt-Exempt-Exempt) status. The EEE in NPS refers to the tax treatment at three main stages.

- Exempt (Contribution) - Contributions made to the NPS Tier-I account qualify for tax deductions under applicable sections of the Income Tax Act. This reduces the individual’s taxable income during the year of contribution.

- Exempt (Growth) - The gains or returns accrued within the NPS account are not subject to annual tax. This is unlike many other investment vehicles. In NPS Tier-I investing, there is no tax on dividends or capital appreciation. This compounding can work its way without dilution by annual taxes.

- Exempt (Withdrawal) - Traditionally, up to 60% of accumulated wealth could be withdrawn tax-free. Now, the recent regulations have permitted up to 80% for private subscribers, with the balance used to purchase annuity for periodic pension income.

Thus, with the EEE model, NPS scheme benefits extend beyond initial tax deductions. These benefits make it a highly effective long-term retirement and tax planning instrument.

Strategic Tips to Optimise Your NPS Portfolio

If you remain in the old tax regime, you can utilise the additional ₹50,000 deduction under Section 80CCD(1B) by contributing to your Tier-I account. This can increase your total eligible deduction to ₹2 lakh per annum.

Similarly, you can also benefit from leveraging employer contributions. You can encourage your organisation to contribute to your NPS account under Section 80CCD(2). This deduction does not count against your 80CCE limit and can enhance your overall tax saving.

You can also align your regime selection with your tax goals. You can compare old vs new regime before finalising tax plans to maximise deductions.

Finally, you can combine the financial goals of retirement planning and tax saving, to work together. You can view the NPS scheme as a long-term retirement instrument rather than a short-term tax tool.

Conclusion

With the NPS scheme, investors can combine retirement planning with their tax saving goals. Its triple tax benefit and EEE treatment can help both immediate tax savings and long-term wealth accumulation.

NPS scheme subscribers can contribute strategically and choose the better suited tax regime to optimise their tax savings while steadily building a retirement corpus. Therefore, they can ensure financial security and enhanced post-retirement income.

Frequently Asked Questions

Q1: What is the NPS triple tax benefit?

The NPS scheme’s triple tax benefit refers to deductions available under Sections 80CCD(1), 80CCD(1B) and 80CCD(2) for contributions to a Tier‑I NPS account

Q2: Can self-employed individuals claim NPS tax deductions?

Yes. Self-employed contributors can claim deductions under Sections 80CCD(1) and 80CCD(1B) subject to applicable limits.

Q3: Is the growth in an NPS account taxable?

No. The returns accrued in an NPS Tier-I account are not taxed annually, allowing the corpus to grow without recurring tax.

Q4: How much of the NPS corpus can be withdrawn at retirement tax-free?

Traditionally, up to 60 per cent of the NPS corpus was tax-free at retirement. Recent PFRDA regulations allow up to 80% lump sum withdrawal for private subscribers (with at least 20% for annuity), but the extra 20% above 60% remains taxable until tax law changes.

Q5: Do tax benefits under NPS apply in the new tax regime?

Under the new tax regime, personal deductions under Sections 80CCD(1) and 80CCD(1B) are not available. However, the employer contributions under Section 80CCD(2) continue to be deductible.

Related Articles